The Importance of Louisiana Directive 219 By Ray Altieri Jr, CPPA

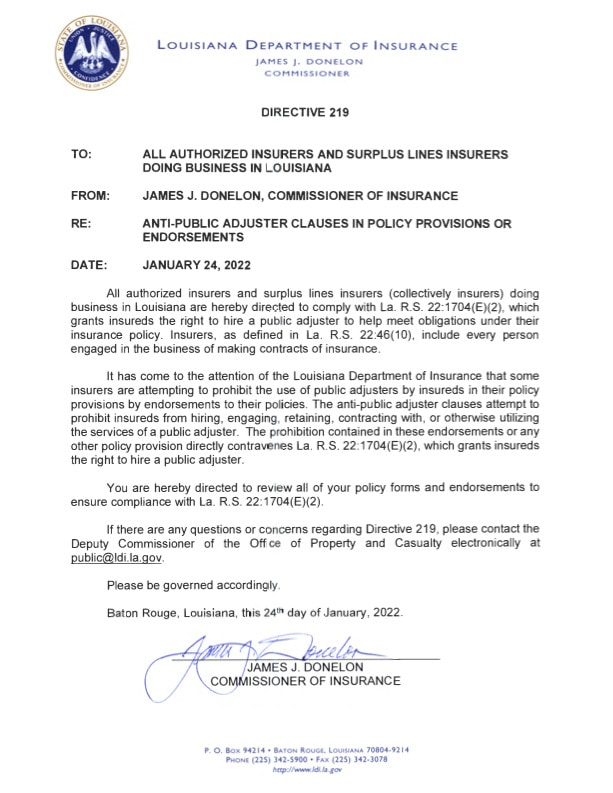

January 24th was a glorious day for policyholders in the State of Louisiana and that glory should be expected to spread to other states as well. What has generated the euphoria is Directive 219. Louisiana’s Commissioner of Insurance issued this directive reaffirming policyholders have the right to hire public insurance adjusters to assist them with their property insurance claims regardless of what insurers quietly insert into the insurance policies of unsuspecting property owners.

This directive is very important because in recent years in multiple states, not just Louisiana, certain insurers have begun inserting endorsements into a property owner’s policy imposing a prohibition against the hiring of public insurance adjusters. These endorsements indicate the hiring of a public adjuster would automatically be grounds to deny a policyholder’s legitimate claim and/or cancel their insurance policy. This underhanded practice is a major afront to all that is fair and honorable in business since it quietly takes away a right from an unsuspecting consumer that he or she may not even know exists. These endorsements cannot be allowed to stand unchallenged because they are anti-consumer. In addition, it most likely may be an unconstitutional restraint of trade when considering public adjusting is a legitimate business/profession, licensed by state governments, who also provide strict oversight.

It is easy to come to the conclusion just how misleading these types of endorsements are. Here is what we know to be true about public adjusting at its most basic level: most people do not know what a public adjuster is or that this type of profession even exists. Policyholders only need us when they need us, therefore public adjusters are almost entirely an unknown entity to the general public, UNLESS AND UNTIL they actually suffer a major loss. This generalized anonymity can cause policyholders to fall prey to the ill effects of such an endorsement without them truly knowing the pitfalls of allowing it on to their insurance policy. Of course, that is if they even know that endorsement is there. For an insurer to be allowed to coax them into giving up a right they know little about, by tempting them at a point when the consumer has no current need or any expectation of having a need, reeks of deception. Imagine the vulnerability of a policyholder (to an insurer) who does not have an option to hire assistance when the insurer goes into the claims adjustment already knowing that vulnerability. Can you imagine the forced settlements they will be subject to or the resulting increase of claims in litigation because of this endorsement? Lawyers and litigation may be a policyholder’s only choice. And if the claim is not financially significant enough for a lawyer to engage?

People naively or at least without much option, have to put their trust into their insurer at the time of policy purchase. They see this insurance policy as their trusted opportunity to be resurrected out of devastation and loss should the major event ever occur—even though most people think: it will never happen to them! Unaware policyholders, (even sophisticated businessowners) will be led down a path to sign for such an endorsement under the lure of a premium discount which unknowingly is to their own detriment. Many people, even those most sophisticated, do not realize they need professional adjusting assistance until well after they interact with their insurers when suffering a loss. Only then, do they realize their incredible disadvantage in the claims process. What happens to those who do not receive a fair analysis or adjustment? Those people do not realize they need help until AFTER their insurer is not providing them with a fair settlement opportunity.

There is no altruistic need for this public adjuster prohibition endorsement other than for an insurer to gain an even more dominant advantage over its policyholders. After all, it is not as if these policyholders are required to hire us after they learn of our existence. So why would a policyholder be prematurely prevented from hiring a licensed professional who meets all State standards to conduct business, under the very government who underwrites that existence? If insurance commissioners are truly protecting policyholders, they must act affirmatively to prevent this scheme from being perpetrated against the insuring public and to prevent the restraint of trade the endorsement imposes upon the government licensed public adjusting industry. By the way, does a policy form like this even prevent an attorney from hiring a public adjuster as an expert on a case based on the language also stating—“otherwise utilize…”?

Every industry has “it’s ying to it’s yang.” The Internal Revenue Service has its agents and tax accountants. Litigation has its plaintiff and defense attorneys. Realtors have their seller and buyer agents. Why would the property insurance company claims adjuster not work with a policyholder claims adjuster in the claims process? There really is only one answer to that question and unfortunately it surely does not benefit the property owner.

Working property claims since 1980 gives me perspective. Perspective gained over the decades of experiencing insurer backlash after major hurricanes strike certain regions of the country. Louisiana has had their share of hurricanes the last couple of years and what does that misfortune produce? It produces endorsements prohibiting the hire of public adjusters. Unfortunately, that is the solution for some insurers. It is time for other State Insurance Commissioners to act and eliminate these endorsements from being inserted into their insurer property policies. Your property owners are counting on it.

Every industry has bad actors. Where there are bad actors in public adjusting, let’s deal with them and their ill-conceived schemes directly like other industries would. Let us refrain from using the “Kill ‘em all and let God sort ‘em out” philosophy. We are grateful to Louisiana Insurance Commissioner Donelon for demonstrating the integrity to see the value of our profession and the benefit it provides to his State’s insured public.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}